The cost of compliance with the EUDR will limit its impact on reducing deforestation (commentary)

Mongabay (23/02/2026) - The production of food continues to eat its way into the world’s tropical forests. Agricultural expansion drives nearly 90% of global deforestation, according to the Food and Agriculture Organization of the United Nations (FAO). The sector therefore represents a critical climate challenge: forest loss and degradation account for about 11% of global greenhouse gas emissions, by estimates from the Intergovernmental Panel on Climate Change.

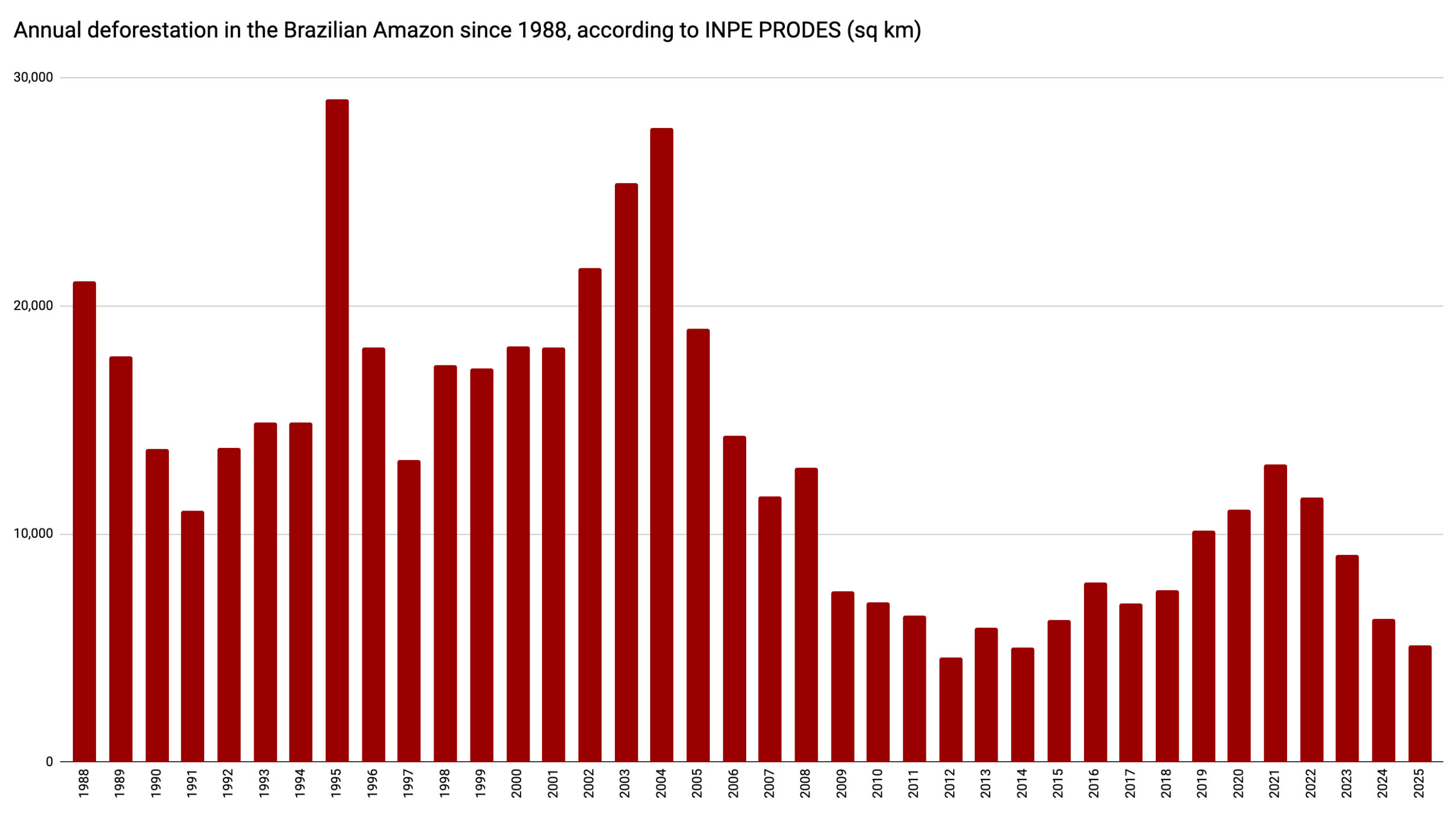

One primary strategy to slow deforestation over the past two decades involves food and agri-commodity companies pledging “zero deforestation supply chains”, under pressure from consumers and environmental groups. These commitments have helped reduce deforestation from land uses like soybean production in the Brazilian Amazon through initiatives such as the now-suspended “Brazilian Soy Moratorium”. Tropical deforestation globally has remained persistently high, however.

We argue here that the long-term impact of “zero deforestation supply chains” will be limited by the costs of implementing and operating these pledges; companies striving to do their part to reduce deforestation are less price-competitive than those that do not. Adjustments are urgently needed to translate corporate engagement into more collaborative and effective approaches to deforestation.

With the goal of mitigating deforestation, the European Union has adopted a “zero deforestation supply chain” approach as the basis of its Deforestation Regulation (EUDR). When and if it is eventually implemented, the EUDR is set to exclude from the EU market those agri-commodities produced on land deforested after 2020. Implementation, originally scheduled for January 2025, has been postponed twice, however, and its future is unclear. EU countries are increasingly worried about the consequences of too much regulation on their businesses and about the competitiveness of European goods.

If the EUDR is implemented, it will require companies to verify that the seven commodities (palm oil, cattle, soy, coffee, cocoa, timber, rubber and including derived products) included in the EUDR, when placed on the EU market, are produced legally and on farms that did not deforest after December 31, 2020. The EUDR also requires “physical segregation”, meaning compliant commodities must be kept separate from non-compliant commodities at every step of transportation and storage throughout the supply chain until entry to the EU.

This is where most of the added costs come in. Commodities are defined by their interchangeability and are regarded as largely identical no matter where or how they were produced. They are usually traded on international contract terms in vast quantities that reduce the costs of transportation, storage, and market transactions, enabling widespread and efficient international trade. With little product differentiation, competition is predominantly a matter of price. The global trade of soy and palm oil commodities amounts to hundreds of million tons a year. Daily, huge volumes move from farm fields by trucks, then trains, barges, and gigantic seagoing vessels, through warehouses and port terminals to import ports, processing facilities, and feed mills around the globe, through supply chains designed for reliability and cost efficiency.

International agri-commodity trade is big business with low profit margins.

Take soybeans, for example, the world’s primary source of protein for animal feed. It is the high-protein feed ingredient that ensures efficient production of pork, poultry, fish, and dairy products in Europe and across the globe. The global production of soybeans has risen to 426 million metric tons per year, according to the USDA. Forty-one percent of it, 175 million metric tons, is expected to be harvested this year in Brazil, the world’s number one exporter of soybeans. A highly competitive portion of Brazilian soybean exports trades at profit margins of around one percent of the price. The European processor converting soybeans into oil and meal may earn net profits of 2-3 percent of the price (margin and profit estimations based on lead author’s industry experience), ranging in recent years between $350 and $600 per metric ton. Such narrow margins leave very little room to absorb additional costs.

By demanding product segregation in particular, the EUDR will, in effect, de-commodify soy and other agricultural products, and that means higher costs. Warehouses and export terminals will need to invest in additional storage silos, use existing silos less efficiently, or reject non-compliant commodities if the goods are intended for export to the EU.

A realistic assessment of EUDR implementation costs must look beyond administrative overhead and account for the significant upstream expenses incurred in producer countries associated with physical segregation, traceability, and geolocation. These costs accumulate at every stage of the supply chain, threatening the competitiveness of commodities and potentially exceeding the thin profit margins (1–3%) that prevail in certain parts of the soy market. Because they ignore these cumulative factors and dilute the impact across total rather than relevant revenue, some recent estimates of EUDR implementation costs based upon percentage of EU companies’ revenues greatly underestimate these costs.

Determining the exact costs of physically separating commodities can be challenging, as expenses differ between companies and are often kept confidential for competitive reasons. Segregation costs are also volatile and complex to calculate. European trade associations have calculated the additional costs of physical segregation to be up to an additional 25% for transport and storage, which is to say, exorbitant, even if their calculations are somewhat opaque. To illustrate potential costs of physical segregation, they point to the segregated supply chains developed to avoid contamination of non-GMO and organic feed resulting in premiums of non-GMO soybean meal on the German market of 50% or more. For Brazilian soy, the real consequence of the physical segregation requirement is a split export market, increasingly diverting goods away from the EU and onto other global markets led by China.

Some of the companies trading Brazilian soy to Europe will find ways of coping with the additional costs, either by European buyers agreeing to partly cover the costs or by exporters dedicating specific supply chains entirely to EUDR compliance. Still, millions of tons of Brazilian soy will need to pass through narrow, high-competition, low-margin trading points of the supply chain. Feed mills will also look hard for lower priced alternatives. Higher prices in deforestation risk regions will nudge some feed demand to soybeans regions classified as low risk by the EUDR or to raw materials not included in the EUDR, such as canola and sunflower meal. The EUDR applies to all 27 EU countries, but it is open to competitive substitution away from the seven agri-commodities that it covers. Thus, European buyers will likely avoid the most problematic deforestation and conversion areas, and the additional costs may be for naught.

What then, has the potential to make commodity market initiatives more effective in addressing the complex issue of deforestation and forest degradation?

They should first and foremost reinforce public policies and programs in producer regions that currently reduce or have the potential to reduce deforestation.

It is through closer alignment between supply chain strategies and public policies in producer regions that forest protection can become more effective and make actors along the entire agri-commodity supply chain more competitive. When commodities comply with both commercial market standards and strong public policies to address deforestation, trading companies are likely to also grant these states preferred supplier status—a meaningful recognition that forest-progressive states have sought.

Brazil provides an important case study for how market-driven supply chain initiatives have missed opportunities to recognize and reinforce robust forest policies. Notably, by adopting the “zero deforestation” criterion—rather than “zero illegal deforestation” —both the EUDR and the Brazilian Soy Moratorium ignore the legal right held by farmers to clear some of their private farmland under the Brazilian Forest Code (now called the Native Vegetation Protection Law); landholders can clear up to 20% of their farms in the Amazon biome and 65 to 80% in the Cerrado. The NVPL is the world’s most restrictive regulation concerning private land forest protection, albeit not fully implemented. Market-based initiatives that acknowledge the legal rights established under the NVPL increase support for the regulation within the powerful farm sector, reducing the likelihood that the law will be gutted and increasing the likelihood that similar policies will be adopted by other tropical forest nations.

Market initiatives to address deforestation will also have a greater impact if they recognize and reinforce regional progress in slowing deforestation, going beyond the prevailing farm-level performance metric. Brazil launched the Plan for the Prevention and Control of Deforestation (PPCDAM) in 2004 that led to a 78% reduction in Amazon deforestation rates from 2005 through 2012. This historic decline in deforestation was short-lived in part because the Plan was heavy on punitive measures and light on positive incentives; for example, it did not translate into greater access to international markets or other benefits for farmers.

{kind=link}

There is an important opportunity today for corporations to increase the effectiveness of their tropical forest commitments. Over the last 19 years, a UN-backed mechanism called “jurisdictional REDD+” has been developed for funding tropical forest nations and states to establish the public policies and programs, forest monitoring systems, and governance structures for systemically reducing deforestation and forest degradation caused by wildfire and logging across vast territories. A wide range of companies can contribute directly to the success of JREDD+ programs in the regions that grow their agri-commodities by buying their high integrity carbon credits and by recognizing these programs for what they are: large-scale, systemic solutions to deforestation and forest degradation.

The collapse of the Brazilian Soy Moratorium and ongoing delays in the implementation of the EUDR are best seen as warning signs that market sanctions against farmers who legally clear a portion of their land may have the counterproductive effect of weakening strong forest regulations. There are straightforward, large-scale solutions for initiating change and ultimately ending tropical deforestation and forest degradation. Positive change can be achieved if market supply chain initiatives align with and reinforce strong public policies in tropical forest nations to ensure economic viability and competitiveness on both sides.