Cover Story: Commodity boom seen capped in 2H, but plantation stocks may play catch-up

The Edge Markets (08/07/2021) - A strengthening US dollar could put a spoke in the wheel of the global commodity rally in the second half of the year, say analysts.

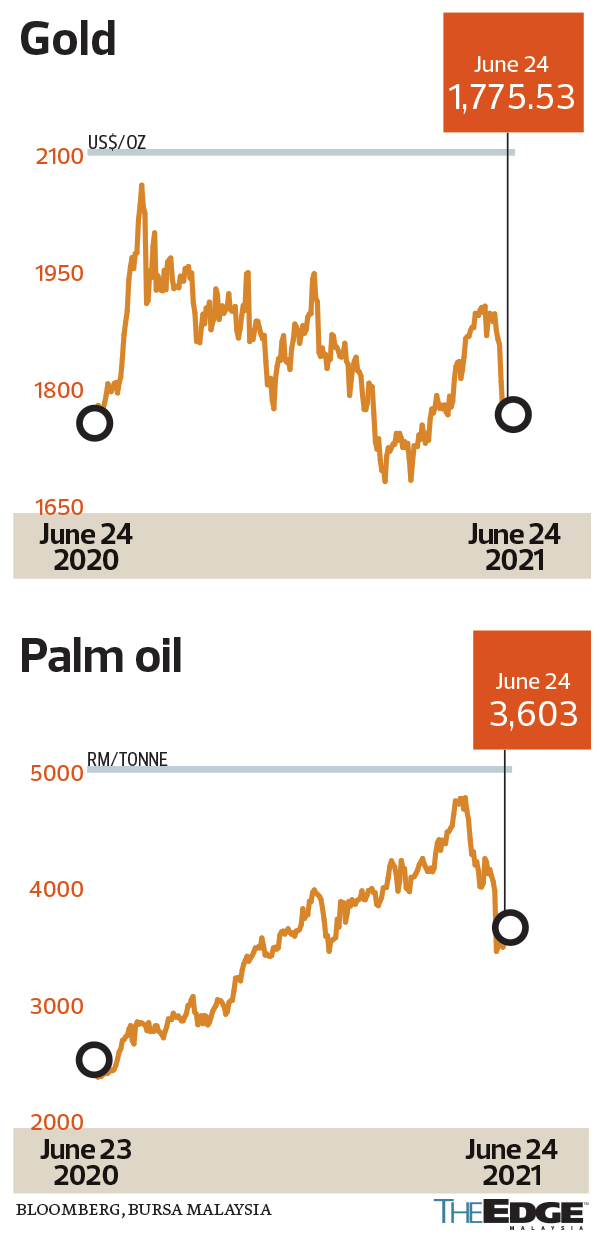

As commodities are typically priced in US dollars, a stronger greenback would make them less affordable. As such, prices of crude palm oil (CPO), which have gained 47.6% in the past year, may be capped for the rest of the year. It hit an intraday high of RM4,800 in May. At the time of writing, the CPO futures contracts for August and September settled at RM3,492 per tonne and RM3,421 per tonne respectively.

Still, analysts believe plantation stocks offer attractive upside potential in the coming months as they have yet to fully appreciate the high CPO prices enjoyed by the market in the first half.

“Earnings from plantation stocks are expected to be good due to the high CPO prices, which could lead to a revaluation catalyst. We believe investors are undervaluing plantation stocks,” MIDF Amanah Investment Bank Bhd research head Imran Yassin Yusof tells The Edge.

Graph: https://assets.theedgemarkets.com/pictures/CS_cht4_TEM1376_theedgemarkets.jpg

{kind=link}

Inter-Pacific Securities head of research Victor Wan agrees, saying that the plantation sector is one of the sectors that will be in focus. He has a “buy” recommendation on Hap Seng Plantations Holdings Bhd and TSH Resources Bhd.

“All commodity prices have probably overshot and eased off a bit. Then again, they will remain elevated. We expect CPO prices to consolidate in the second half,” says Wan.

Imran also likes TSH, noting that the company has not been affected by the recent lapsed land deal. Last Monday, Kuala Lumpur Kepong Bhd (KLK) terminated agreements to acquire two Indonesian firms from TSH due to non-satisfaction of certain conditions.

This came after KLK extended a takeover offer for IJM Plantations Bhd for RM3.10 per share. The not-so-expensive valuations among the plantation players may lead to more mergers and acquisitions.

For big-cap play, Imran prefers KLK, whose net earnings jumped fourfold to RM847.85 million for the six-month period ended March 31, 2021.

Although the plantation sector has been impacted by environmental, social and governance (ESG) issues, Imran highlights that the ESG ratings done by FTSE Russell and Bursa Malaysia on plantation stocks are quite good.

OCBC Bank expects Malaysian Palm Oil Board’s (MPOB) ending stock to trend below two million tonnes through 2021, fuelled by continued supply disruptions due to the Covid-19 situation as well as the increasing need to replenish vegoil stocks in China and India.

“The broad decline in the soybean complex, however, may cap further gains in palm,” it said in its Commodity Outlook 2021 report issued on June 15.

As for the steel sector, Kenanga Research analyst Lum Joe Shen is of the view that demand will remain robust on the back of the reopening of the economy. Furthermore, supply will be constricted to a certain degree as China prioritises carbon neutrality.

“Moving forward, steel prices will be more stable. We won’t see a sudden uptrend momentum, which happened in the past few quarters.”

As earnings for steel companies are likely to have come off, he expects their share prices to trade sideways in tandem with normalised valuations.

“1Q was probably the best quarter for steel players … But prices won’t fall sharply as the supply-demand dynamics are still favourable,” says Lum.

While China’s import of iron ore — the main raw material in steel production — may slow in the next six to nine months, OCBC says this does not mean its appetite for steel has waned. “Its shifting stance towards prioritising pollution control means it wants to encourage a more efficient pickup and recycling of domestic steel production, that is, encouraging less steel exports and importing more foreign scrap steel. Once inventories dwindle, however, we expect China to return to international markets to replenish its stock.”

Iron ore is the second largest commodity in the world by weight and value, after crude oil.

As for gold, UOB says most of the positive drivers for gold remain valid, including a strong rebound in China’s gold jewellery demand, slowdown in outflows from gold exchange-traded funds and relative weakness in Bitcoin resulting in the pullback of the Bitcoin versus gold ratio.

“Going forward, if inflation rises further, real yield may well head further south. This is where gold can draw strength from its traditional demand as a hedge against inflation. But the US Federal Reserve’s (plan) to bring forward its rate hiking cycle into 2023 has stopped gold’s 2Q rally in its tracks.

“While we stay positive for gold, any potential upside strength is now limited and curtailed. Overall, we lower our gold forecast and now see gold topping out at US$1,900 per ounce in 1H2022.”

Gold price broke the US$2,000 per ounce level in August last year. However, it has slipped 6.5% year to date.

Read more at https://www.theedgemarkets.com/article/cover-story-commodity-boom-seen-capped-2h-plantation-stocks-may-play-catchup